The 2023 Guide to Debt Management Plans – Chapter 1

Wondering when the correct time is to seek help with a debt problem? The answer is, the sooner the better. Read on with Cashfloat to see when and how you should seek help to deal with debt.

- The first step to dealing with debt is calculating how much you actually owe.

- If you seek outside help, you will be guided in making a formal or informal arrangement with your creditors.

Cashfloat is a leading payday-loan lender in the UK. Unlike other lenders, Cashfloat is customer oriented. Our customers’ safety is at the heart of our business. Short term loans are NOT a solution to long term financial difficulty! If you are experiencing problems with debt, there are steps you can take to deal with the situation.

In this article, we will guide you as to when you should seek help with debt and who to go to for help. We will also briefly explain some of the common ways of dealing with debt, which a debt advisor may suggest to you.

Don’t Ignore Your Debts

The most important thing, when it comes to dealing with debt, is to start early. Sadly, many people who are in debt put their heads in the sand and hope that the problem will go away. Unfortunately, this won’t happen. It is important not to freeze or panic, but to confront the problem and deal with it, before it gets worse.

Often, the first step is to make a list of all your creditors and work out how much you owe to each of them and what the repayment conditions are. After this, you can work out which of your debts are the most urgent. Knowing exactly what the extent of the problem is will often help you to relax. If you have enough money spare to deal with urgent debts, like your mortgage or rent straight away, then that is a good start.

As we will explain in this article, while urgent debts are the most important, you should also take steps to tackle your less urgent debts. Even if non-payment of certain debts won’t cause you to lose your home, it can still cause you a serious problem. Some people will be able to overcome debt problems by careful budgeting and by sticking to a repayment schedule. Other people will need to seek outside help. Help with debt is available from a number of places. Usually, the best place to go for help is to one of the charitable organisations which help people to tackle debt. The solution they recommend will depend on your circumstances and the severity of your debt. Many of these organisations will also lead people through the whole process of dealing with debt.

Don’t Get Further Into Debt

If you have a problem with debt it is important that you don’t make the situation worse by borrowing even more. When your debts have got to the point where you are finding it difficult to repay them, this is the time to cut back on borrowing and to save money so that you can repay your debts.

Beware of Debt Management Companies

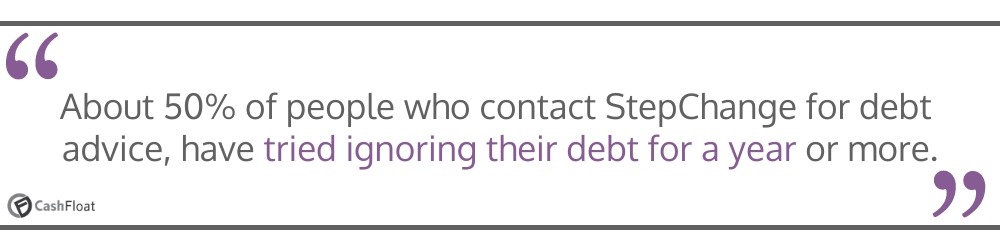

If you are new to the process of dealing with debt, you may be unfamiliar with debt management companies. There are many profit making businesses which offer services to people who are dealing with debt. These companies charge money to people who are already in debt, effectively making their debt situation worse and, often, the debt solutions they provide are available for free elsewhere. It is always better to go to one of the free organisations, such as StepChange, if you are looking for help to deal with debt.

Do You Have a Problem With Debt?

If you are unsure whether you have a debt problem, there are some questions you can ask yourself to understand whether you do or not:

- Are your monthly debt payments such that you are just about surviving?

- Do you know exactly how much you owe?

- Do you lie awake worrying about the next bill that is due?

- Have you left monthly credit card statements unopened?

- Are you failing to make debt payments?

- Are you constantly looking to borrow more to pay off debt?

- Do you panic when you try to plan future spending?

If the answer to these questions is yes, then you should deal with your debts sooner rather than later.

Confront the Situation

The first step in dealing with debt is to confront the situation.

Work Out How Much Money You Owe

Making a list of all your creditors and exactly how much you owe to each of them will help you to see the bigger picture. If you are able to compile all the names and addresses of the companies or people you owe money to, with relevant reference numbers, this will help you with arrangements further down the line. If you still have them you should also find copies of the agreements you made when you borrowed money. File all of this information alongside any recent correspondence you have had for payments you have failed to make, if you have done so.

After this, you will need to work out what payments you will need to make in order to clear your debts, taking interest and other charges into account. The amount that you will have to repay will give you your first indication of whether or not you will need to seek outside help in order to deal with the problem or not.

Priority and Non-Priority Debts

It is essential to make payments for priority debts before you pay your non-priority debts. Priority debts are debts which will cause you the most serious problems if you fail to make repayments. These are usually mortgages or rent payments that are overdue, utility bills, council tax arrears, court fines, child maintenance payments or income tax. Priority debts are often debts which are secured against an asset of yours. Mortgages are secured against a person’s home and these are classed as priority debts because failure to make mortgage payments could cause a person to lose their home.

Non-priority debts are debts for which the consequences of missing payments are less severe. Although they may cause you a lot of worry and, while there are still consequences for not paying them, they can be put lower down on the list when it comes to making repayments.

Non-priority debts are debts like student loans, benefit overpayments, short-term loans, personal loans from family or friends and credit card bills. These are usually debts which are not secured against an asset of yours, such as your house or your car. While they may be significant debts and while you should still do your utmost to repay them, the consequences for missing repayments are less immediately serious. Also, there is often room for negotiation with your creditor when it comes to making payments.

Why You Should Still Deal With Non-Priority Debts

Although it is important to pay your priority debts first and while there is often room for manoeuvre when it comes to non-priority debts, you should still take steps to tackle them. Ultimately, creditors for non-priority debts could take you to court and get a court order that allows them to send bailiffs to your home. While the process is more complicated than with a secured loan, creditors for unsecured loans could take your possessions. On top of this, your credit rating will be badly damaged and there could be other consequences as well if you do not take steps to begin making repayments.

Know Your Rights

It is very important to know what rights you have when you are in debt. The Citizens Advice Bureau has comprehensive advice and information that can help you to understand what your creditors can and can’t do when you are in debt. Often creditors will apply as much pressure as possible and knowing what can and what cannot happen may help to lift the burden of worry.

Often, when you are in debt, confronting the situation and learning how much you owe and what is likely to happen will help to ease your worries. Knowledge is power and, in this instance, knowing where you stand can help you begin to get to grips with your debt.

Make a Plan How To Deal With The Situation

When you have worked out what repayments you will have to make and made a list of your priority debts, you can budget yourself and see how easy it will be to repay your debts. If you can budget yourself to leave enough spare money, it may be feasible to pay off your debts without resorting to outside help.

Do You Need Help to Clear Your Debt?

If you believe that you are able to and you would like to, you may be able to deal with your debt problem without any outside help.

There is a lot of information available on how to create a budget and how to stick to it. If you are able to budget yourself and to leave enough spare money to pay off your debts, then this is the easiest option. If you are unable to do so or if you think that you will struggle to meet repayments, then you should seek outside help.

Getting Debt Help

If you do decide to seek outside help, remember that it is always best to go to one of the free charitable organisations which help people to deal with debt, such as StepChange or National Debtline. These organisations will be able to recommend the best course of action for you to take and many of them will be able to lead you through the whole process of clearing your debts.

Often, this will mean making an arrangement with your creditors. Arrangements can be either formal or informal.

Formal And Informal Arrangements

Informal Arrangements

If you do have some money available to pay off your debts then it is often possible to make an informal arrangement with your creditors. Debt management plans, which this whole guide is devoted to, are an example of an informal arrangement. Alternatively, if your creditors agree to it, you may be able to take a payment holiday, pay less interest on what you owe, have the total amount that you owe reduced or reach another arrangement.

The consequences, if you owe money, to making an informal arrangement are usually less severe than with a formal arrangement. Usually, they will allow you to clear your debts under conditions which are possible to meet. The difference between formal and informal arrangements is that informal arrangements are not legally binding. While they have the bonus that the arrangement will not be marked on your financial record, your creditors are not legally obliged to meet the conditions of it. This means that they could still pursue you for money and take legal action to reclaim it at a later date.

Formal Arrangements

Formal arrangements are usually sought when a debtor is unable to reach an agreement with their creditors or when debt levels are so high that it is impossible for a person to repay what they owe. Usually the consequences of making a formal arrangement are more severe for the person who owes money. On top of this, creditors are often unable to reclaim their money.

In many cases, both the person who owes money and their creditor will prefer to make an informal arrangement than to pursue a formal course of action.

What are Debt Management Plans?

As we mentioned earlier, debt management plans are a type of informal arrangement which you can make with your creditors to pay off your debts. The rest of this guide discusses debt management plans in depth.

Normally, debt management plans are arranged by a third party debt management plan provider. This third party will negotiate, on behalf of someone who owes money, reduced repayment rates with creditors. Under a debt management plan, repayments can be reduced to an affordable rate. Where previously a debtor was unable to make repayments, under a debt management plan, they will be able to meet the repayment conditions. Payments are usually made as one single payment to the plan provider, rather than as several payments to the various creditors. For an in-depth explanation of how debt management plans work, go to this article here.

Alternative Ways to Deal With Debt

Besides debt management plans, there are many other formal and informal debt solutions which are available. Before you embark on any debt solution, it is important that you seek professional and impartial advice and make sure that the solution you are choosing is the best one for your circumstances.

Other solutions to debt include:

- Individual voluntary arrangements (IVAs)

- Remortgaging

- Making a settlement offer

- Debt Relief Orders

- Debt consolidation

- Administration orders

- Bankruptcy

It is important to remember that bankruptcy and other more serious debt solutions are only necessary in extreme cases of debt. Remember to avoid debt management companies when you are seeking advice on how to deal with debt. Alternatively, go to one of the debt management charities, such as Christians Against Poverty.

In Summary…

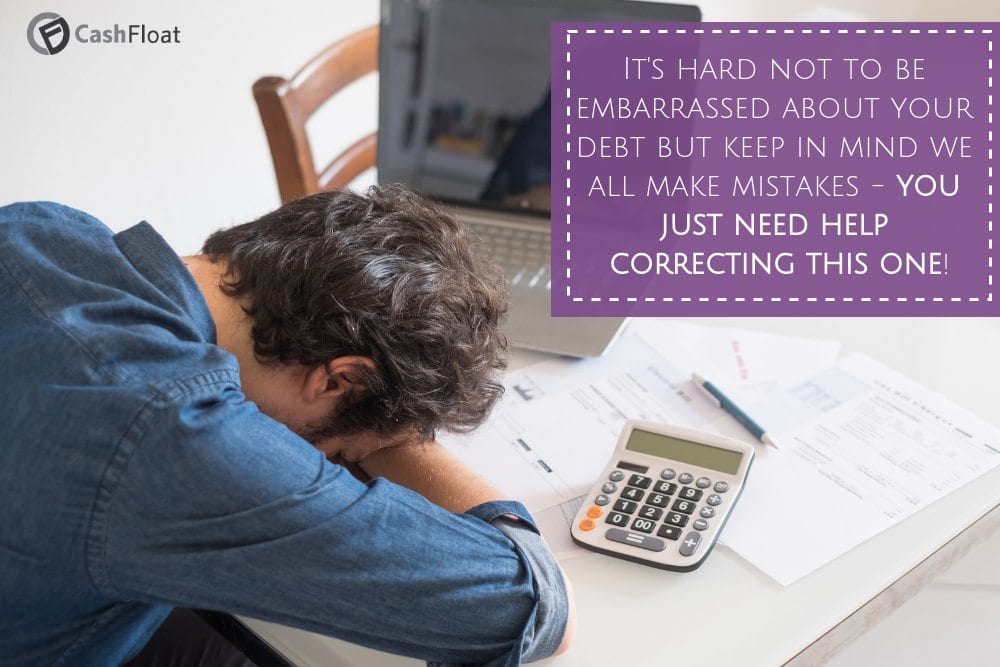

The most important thing to remember, when it comes to debt, is that you should do something about it. It can be embarrassing to ask for help, but the problem will only get worse if you ignore it. It’s easy to pretend to yourself that everything’s fine, but you should be honest with yourself about whether it is or not. While it may seem difficult at first, it’s always possible to climb out of debt.

If, after you have looked at how much you owe, you decide that you need help, remember that asking for help is not a shameful thing to do. There are many organisations which are ready and willing to give you assistance and receiving professional and impartial advice will help you to choose the right course of action. This advice can be found for free from one of the many debt charities in the UK.

Even before the coronavirus pandemic, around 8.6 million people in the UK had a high level of debt and the problem has been made much worse by coronavirus. Debt is not an uncommon problem and there are many ways to deal with it. Debt management plans are one of the most common ways that people deal with debt and the rest of this guide explains, in depth, how they work. Read on to find out more.