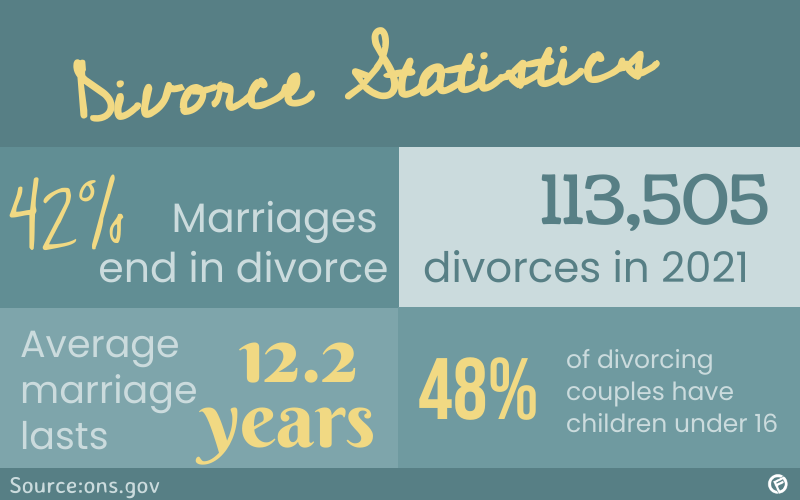

Full Guide to Managing Family Finances – Chapter 10

Ideally, divorcing and separating couples will be able to reach a fair agreement with each other without resorting to the courts. Cashfloat explores what to think about when dividing responsibilities and assets in the UK.

What is a divorce settlement, and do I need one?

If you and your partner plan to divorce, it is a good idea to try to agree – as soon as possible – what will happen with respect to the home and other shared assets (such as bank accounts). When this is a formal legal agreement, it is known as a divorce settlement. Assets it will cover include:

We have children. What else should we agree on?

If there is a child, or more than one child, and one of the parents does not live with that child, then a child maintenance agreement is made to help cover the child’s living costs. This can be arranged privately between the parents or through the Child Maintenance Service.

You will also want to agree custodial arrangements, and how and when the other parent can see their child.

What happens to the family home?

The family home is usually the biggest asset that a couple will have and there are a number of ways to deal with this asset:

If there is enough equity in the house you can sell it and split the proceeds so that each partner can buy another home.

One person can buy the other one out.The person who stays in the house needs to transfer the mortgage into their own name. This is only an option if the sole owner can afford to make the repayments. They may need to rely on online loans in order to keep up with the repayments.

It is possible to delay a sale, actioning this much later. However, this ‘locks in’ whatever equity the join owners have in the house.

The courts also have the power to prevent the sale of a home until the youngest child has reached the age of 18. This allows stability and continuity for the children until they are adults. If the couple are unable to agree on a course of action, the courts will decide. They always try to put the interests of the children first.

Breaking Up a Joint Mortgage

Sorting out a joint mortgage is an important issue that you need to tackle when a divorce is in progress. If the absent partner remains on the mortgage it will be hard for them to start a new life and buy another property. So, if possible, transfer the family home into the name of the person who remains living in it. It also means that once you break the financial tie, there will be no joint credit files (and if your ex partner defaults on a loan, it will no longer affect your credit report). Of course, the person staying in the house will face financial tests. This will show that they can afford to make the full repayments before the mortgage company transfers the house to their name.

Lone parents who are unable to afford a mortgage can consider asking for a guarantor mortgage i.e. from a close relative. For all parties it is in their best interest to achieve a clean break financially when they divorce. As long as this happens there is no chance of one party coming back for more should the other one have a big improvement in their lifestyle. e.g. they start a new business that flourishes.

Joint bank accounts and insurance policies

Some couples do not have much in the way of assets. However, there are still a number of financial products such as savings or bank accounts, insurance policies, and joint loans that need considering. If you are able to have the conversation with your partner in an equitable manner then you can deal with these kinds of issues easily and quickly. However, if this is not the case you need to make sure that your ex does not start to run up bills in joint names, take out large and expensive personal loans or default on loan repayments – especially payday loan repayments which can easily spiral. Unfortunately, this could have an adverse effect on your future financial credibility.

In any event, you should contact all financial institutions as soon as possible to advise them that you are divorcing. Your financial institutions may advise you to give authorisation so that both of you have to sign for an overdraft or any other payments from the joint account. If there are savings you should always ask for two signatures so that your ex can’t empty the account before you get your share.

We recommend you:

- If your salary goes into a joint account then you should ask your employer to change the payments to a single name account

- Make sure that any joint internet or telephone banking facilities are frozen until things are legally sorted out

- In extreme conditions you can ask for a joint account to be frozen but this may put regular payments for bills at risk and could affect your future credit score

There are rules about joint savings accounts for people who live in England and Wales. These rules state that funds in a joint account belong to the account holder who paid it in. However, in some circumstances a partner can make a claim for part of the savings even if they did not pay it in directly. This is because many women give up work to run the family home. Therefore, it entitles them to a fair share of what the ex-partner accumulated during the marriage. Different rules apply in Scotland and Northern Ireland. Funds in a savings account there are distributed equally to the joint account holders.

Credit cards and store cards

For credit cards and store cards, each person on the joint account is responsible. This means that if your partner goes on a spending spree with that card you will still be liable to pay it all back. That is why it is so important to quickly notify companies and close joint credit accounts. With home insurance policies or car insurance where one of the parties is a named driver you will have to write and ask them to take you or your ex off the policy.

Finally, you should share bills, for the former family home, equally – up to the date you or your ex move out. So, take meter readings and then change the account into a sole name. You can usually do either over the telephone or online.

Personal possessions

Most couples can decide what to do with personal possessions quite easily. One may decide they don’t want anything except books and music. Or they may decide they need some furniture (or at least a bed) to start again. If deciding who gets what has become impossible and compromise is not forthcoming on both sides you should make a list of all items and try to come to an agreement by ticking them off one by one. Making a decision about dividing furniture and household goods may seem mercenary. However, both parties have to begin new lives, and it is unfair for one party to have to buy everything when they move to a new home.

Here are some general guidelines when dividing personal possessions:

- The person who purchased the item owns it

- Joint purchases – it is possible to pay for the other half, that is, reimburse the other for it

- A present belongs to the recipient. Don’t try to claim back gifts.

- Value valuable items like paintings or a collection can be deemed family assets to divide as part of the divorce settlement.

Pensions

After property, pensions are usually the biggest asset, and these can be split between both parties if it is felt one partner has a lot more than another. There is also the case when a wife has stayed at home to raise children and may not have a large pension pot. In this instance the court can rule that some of the husband’s accrued pension is transferable to the wife. All pensions except the government ones are taken into account. This area of the divorce settlement is fraught with many difficulties. It is therefore best to consult either a divorce solicitor or a financial advisor. Only a court can make a sharing order for pensions. So, if you can’t agree this will be part of the divorce financial settlement that the court decides before they issue the decree nisi.

Here are four options:

Sharing the Pension

It is possible to share the pension(s) with one party getting a percentage of their partner’s pension assets. The amount agreed upon can be transferred into a pension fund that already exists. Alternatively, the partner receives the shared amount and can start up a pension to deposit the funds. You cannot have a share of a pension as a cash sum and it must be put into another pension fund.

Value the Pensions

The second option is to come to an agreement that the value of pensions will be offset against any other assets like the family home. You may come to a pension divorce settlement that one partner will get a larger share in the equity of the family home instead of having a share of the other party’s pension funds.

Deferred pension sharing

There is also the option of deferred pension sharing. This comes into effect when one partner has already retired and the other is too young to receive a pension of their own. The divorce settlement involves sharing the pension at a later date when the younger partner is ready for retirement. It is a more complex agreement. We suggest you avoid it whenever possible. The legal fees to make this kind of arrangement are considerably higher. It also means that there is no clean financial break after the divorce.

Since most people wish to move on with their lives this is not the ideal solution. However people use this option when one partner is a lot wealthier than the other. In some cases the court will grant one partner a deferred lump sum payment. For instance, a sum the pension company will pay to the ex when the partner actually retires and claims their pension.

Pension Attachment Order

And finally, you may ask for a pension attachment or earmarking order. This means that when your partner does retire you can get an income from their pension, which can sometimes drastically increase your own income, leaving you much more financially independent and more able to cover all expenses without needing online loans or other sources of credit as you may have needed before.

For couples who have retired and then want to divorce the rules are different. You can claim an income from a pension but not part of a lump sum payout. Want to know more about pensions? If you want to read more about your own pension, you can read our pension guide here.

Conclusion

In conclusion, navigating the complexities of divorce settlements can be challenging, but with careful planning and consideration, it is possible to reach a fair and amicable agreement. Prioritizing open communication, seeking professional advice, and understanding the legal implications are crucial steps towards achieving a favorable outcome. Remember to evaluate your financial situation, assess your needs, and strive for a balanced division of assets to secure a stable financial future after divorce.