Buying a house for your child is a great way to invest for their future. Learn with Cashfloat how to ensure that your child gains the most from your investments and that they have a secure future.

- Find out if you can buy a house and put it in your child’s name

- The best way to invest in a house for your child is to form a trust

- Forming a trust is a legitimate way to invest without having to pay capital gains tax or inheritance tax.

One of the simplest ways to make an investment for your child’s future is to buy a second property. It can give them somewhere to live, help them save money on rent and could prevent them from relying on wage day advance loans every month!

When you purchase a property for your child, it’s important to minimise the amount of taxes and fees you pay when you initially purchase it. Also, when the time comes for them to inherit it’s important that you have done everything to minimise the amount of inheritance tax that they will have to pay.

In this article, Cashfloat will explore the different ways that you can buy a property for your child.

1. Buying a House and Putting it in Your Child’s Name

Buying a house and putting it in your child’s name is an option, but the complications and costs which are involved usually make it simpler to gift a child money in order to buy their own house.

As with gifting your child money, you need to consider the possibility of inheritance tax being owed in the future and also the possibility that your child may become divorced.

On top of that, if you buy the house yourself, rather than giving your child the money to do it, then you will probably have to pay stamp duty and capital gains tax on the purchase. Your children won’t need to pay this if they are first time buyers.

To add more complication, you will have to go through the conveyancing process when you transfer the property to your child. This can be complicated and will add further costs. In summary, it’s simpler and cheaper to gift your child money to buy their own house, rather than buying one for them and transferring ownership to them.

Who are we?

We’re Cashfloat, a premium payday loans and personal loans provider in the UK. We provides loans that are designed to help people in emergency situations who can’t make it to payday. Our loans are expensive, which is why we try our best to maintain a blog about money and personal finance so that less people end up needing our loans. We hope you find this article interesting!

At Cashfloat, we are not currently offering mortgages (maybe one day soon!) However, there are so many more costs involved in buying a house besides the actual price of the house. Even if your parents are helping you out with the cost of the home, they may not help you with the other expenses that can crop up, like:

- Stamp duty

- Valuation fee

- Surveyor’s fee

- Legal fees

- Electronic transfer fee

- Estate agent’s fee

- Mortgage fees

- Costs of moving home

- Ongoing costs to your new home

These expenses can amount to thousands of pounds and can be a real blow to your budget. Sometimes a small personal loan can help to cover these expenses. A Cashfloat unsecured small personal loan may be the perfect thing for you! Our personal loans range from £1,000 up to £2,500. Apply today and if approved get the money within an hour.

How much do you need?

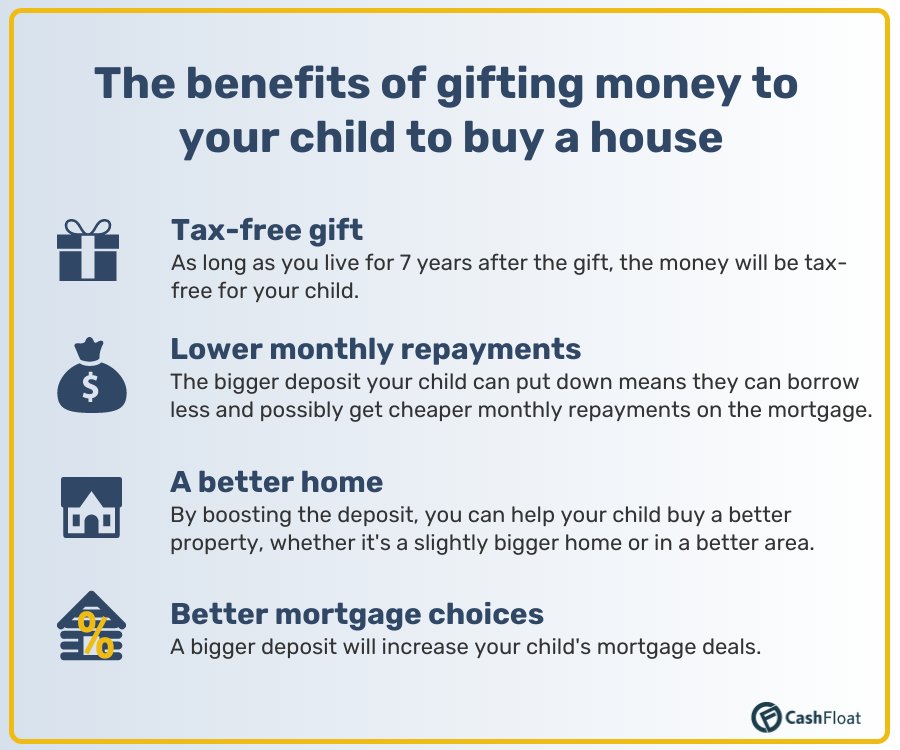

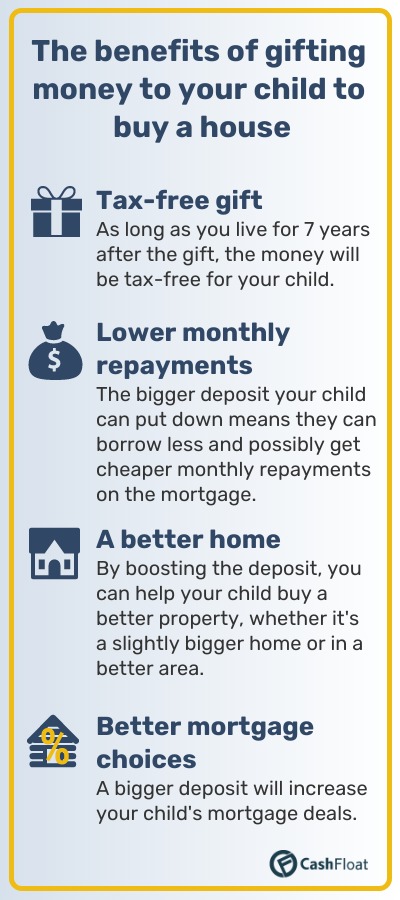

2. Gifting your Child Money to Buy a House

The simplest way to buy a house for your child is by gifting them money to buy it themselves. This would seem like the obvious solution. There are serious tax implications to consider, though, and it is important that you make a distinction between gifting money to your child and loaning it to them. You’ll also need to consider the possibility that your child may divorce from their partner.

Is the money a loan or a gift?When your child applies for their mortgage, they will have to declare whether any money received from you is a loan or a gift. If the money your child has received from you is a loan, then it will affect the mortgage deal that the bank will provide them with. If you, or your child, falsely declare a loan as a gift then you will be committing mortgage fraud.

In summary, if you decide to gift your child money to buy a house, then it has to be a true gift with no repayments.

Inheritance tax

Inheritance tax is another serious consideration that parents have to make when gifting their child money to buy a house. Luckily, neither parents or children will have to pay any immediate tax on the gifted money. However, the money may eventually be liable for inheritance tax.

If a parent who gifts money to their child dies within 7 years of giving the money then it may be liable to inheritance tax. That person’s whole estate, which includes the gifted money, will be totalled up upon their death. If the value is over £325,000, then anything in excess of £325,000 is liable to inheritance tax. The taxed amount could include the gift that your child has received to buy their house.

The amount of inheritance tax that is due on the gifted money is reduced according to the time that passes between the gift being received and the person’s death.

If the time between the gift and the person’s death is less than 3 years, then it will be liable to 40% tax. This amount decreases each year after that, down to 8% after 6 years. After 7 years it will not be liable to inheritance tax.

DivorceIf you gift your child money to buy a house and they eventually end up divorcing their partner, then the house could be split with their partner after the divorce. This is a serious consideration because it means that your investment which is intended for your child could end up being split with someone else.

Some good news if you just need to help with a depositIf you don’t need to loan your child a large amount of money and, instead, you just want to gift them enough to put down a deposit then there is some good inheritance tax news. Each parent is allowed to gift up to £3,000 per year, without it being liable for inheritance tax. If you have not gifted any money in the previous year, then you can also gift your allowance for that year as well.

That means that 2 parents can gift up to £12,000 in a single year without it being liable for inheritance tax. This could be enough to help out with or even secure a deposit. Be careful though, as your gifted allowance also includes money that you gift to other people.

3. Buying a Property in a Trust For Your Child

Buying a property in a trust is usually the best way to buy a property for your child. This is a legitimate way to avoid paying capital gains tax and inheritance tax. However, it can be complicated. Here, we’ll explain how it works.

By setting up a trust, you can avoid paying capital gains tax and inheritance tax when you buy a home for your child. Your child will be able to live rent-free as an adult and will eventually inherit a property. The changes in legislation for capital gains tax now mean that this is an opportunity available to all parents who want to invest in their child’s future.

How to set up a Trust to Buy a Property

Ideally, you should set up a trust before choosing a property to buy. You need to name either one or both parents as trustees. The costs for this part of the deal are minimal and will only set you back a few hundred pounds. Then, instead of buying the house yourself, you lend the deposit money to the trust fund. The trust then makes the purchase using a mortgage. Banks will usually ask for you to be a guarantor for the funds.

There are two types of trust available for this investment opportunity:

Types of trusts |

|

A life interest trust can be set up with a named child as the beneficiary. This means the person named will receive any profit made by renting out the house. Alternatively, you can name two or more children in a discretionary trust. This means that the trust does not automatically give income to the beneficiaries. But, there is more flexibility in this kind of trust document. So, as life tenants, who are able to live rent free, the beneficiaries of a discretionary trust can change. That is, one child can occupy the house for a number of years and then another one can take over the tenancy.

Whichever kind of trust you set up, the beneficiaries have the right to live in the property without paying rent. They are called life tenants. As the children are beneficiaries of a trust, they are considered to have their own property. This means they pay no capital gains tax on a personal private residence.

Advantages of a Trust FundWhen the time arrives to sell the property, there is no capital gains tax to pay. This is as long as you can prove that the beneficiaries of the trust have lived there continuously whilst the property has been in the name of the trust. You do not even have to pay income tax on the sale proceeds. If the house is left empty, you can still avoid capital gains tax for at least 18 months. This allows you a reasonable window of opportunity to sell the property. Once this period of time has elapsed you may be liable for some tax.

There may be circumstances where you already own a second property and want to take advantage of a trust to avoid capital gains tax. In this instance, you can still set up a trust that is called an implied trust. Make sure to let the tax authorities know if your children are occupying the property. Then, you can still action the trust status.

Additionally, if your children want to share the accommodation with friends, it does not necessarily mean that you will have to pay tax. As long as the rent that your friend pays is paid to the trust, they will assess it as rental income. There are some allowances before income tax will be due. i.e. you can claim expenses and mortgage payments before any tax has to be paid on the income. And, if your child is not earning any other amount of income and the rental income does not exceed their personal allowance, there may be no tax to pay at all.

Other Tax Liabilities when Setting up a Trust Fund for Your Child

If you have purchased the property correctly and donated the initial deposit to the trust and the mortgage is set up in the name of the trust there will be no inheritance tax to pay, should you die. But, there are limits to the amount involved. So, if the amount donated is more than the latest allowance of £325,000 then there will be a 20% excess to pay on the residue of the amount. This only applies to money gifted to the trust so unless you are buying a house for your child worth hundreds of thousands of pounds it is very unlikely that the gifted money would count towards inheritance tax. Sums of money that you loan to the trust do not attract inheritance tax.

In the event of the death of one or both trustees, you can appoint new trustees so that the trust can operate as normal. However, if the conditions of the trust specify that the children will inherit the property on the death of the trustees, then normal rules for inheritance tax apply.

Getting Help with Setting up a Family Trust to Buy Property

Buying a house for your child may seem like a complicated procedure. However, a financial advisor or solicitor will be able to help you set up this kind of trust. Imagine the benefits of buying a house for your child! They would have somewhere to live rent free whilst they study or start their first job. They may never have to rely on small same day loans. This will greatly reduce the often overwhelming amount of expenses that young adults face when they move out into the real world. It can also make them more likely to be able to make sensible financial decisions and not get caught in the trap of short term loans to stretch their income.

Conclusion – Buying a house for your child using a trust fund

You can use this system for a short or a longer period of time and as an investment in your child’s future. It has a lot to recommend it! Not only will you be helping your child to be able to save a deposit for a first home of their own, but once you sell the property, you can also reap the benefits of a long term investment. You can put the proceeds into buying a house for your child or you can spend them yourself. We hope that this short article has helped you to make some decisions when buying a house for your child and saving for your child’s future.

4. Loaning your Child Money to Buy a House

Just like when you gift money to your child to buy a property, it is important that you make it clear that any money you lend to your child is a loan. Your child will have to declare any loan that they receive from you to their mortgage providers, otherwise they will be committing mortgage fraud. You will need to draw up the loan with a solicitor and arrange a monthly interest rate and a repayment schedule.

Can loaning your child money help with buying a house?

Loaning money to your child to buy a house can help. You can charge less interest on the loan than they would find elsewhere and you can set up favourable repayment conditions.

However, they will still have debt and it can limit the mortgage options that your child has. Their mortgage lenders will have to take into account the fact that they owe you money and this will affect the mortgage that they will be able to provide. Some mortgage lenders won’t even accept borrowed deposits for mortgages.

5. Taking out a Joint Mortgage with your Child

One choice that a lot of people make is to take out a joint mortgage with their child. Like other ways to help your child to have a house in their name, though, this method has its pros and cons.

What are the upsides?

When you apply for a joint mortgage with your child, the mortgage provider that you apply to will consider both of your incomes. This dramatically increases your buying power and it is often much easier to get a mortgage and to buy a house.

What are the downsides?Unfortunately, this option does have its downsides.

The first one is that if either you or your child become unable to make payments on the mortgage, then the other party may be liable for the whole mortgage. If you become unable to make payments for any reason, then you could land your child in a difficult situation. Likewise, if they become unable to make payments, then you may be liable for the rest of the mortgage. This could put your home at risk if you have used it to secure the mortgage.

The other major downside is that unless you are first time buyers yourself, then taking out a joint mortgage with your child will make the mortgage eligible for stamp duty. You will also have to pay the second home surcharge as well. This will add to the cost of securing a mortgage.

Taking out a joint mortgage will also mean that your credit reports become linked. If either you or your child have bad credit, then this may affect the other party’s ability to secure financial products.

On top of this, you and your child will have to agree with each other about when and for how much the property should be sold in future. This can be a source of disagreement.

What Other Ways Are There To Help Your Child Buy a House?

On top of all the ways we have suggested, you can also act as a guarantor for your child’s mortgage or you can use equity release. Have a read of these articles for some information on these options:

- Equity release: how it works and the risks involved – MoneySavingExpert

- Guarantor mortgages – Which?