In this article, Cashfloat – a responsible personal loan direct lender – will look at how banks used to approve mortgage applications before the banking crisis. This will help us understand how mortgages affected the banking crisis in the UK.

Pre-Banking-Crisis Mortgage Rules

Before banks started to focus on maximising their profits, mortgages were quite strictly controlled. Loans for house purchases were subject to approval. You could get approval only:

- After a search on the property

- A comprehensive financial audit on the potential borrower.

- If you could prove you could make the repayments

- If you had a regular job

- You wanted to borrow a maximum of two and half times your annual salary

In addition to these rules, borrowers had to give a deposit between 10% and 20% of the mortgage value. This gave the lender a measure of security in case of a default. In general, you could only get a 90% mortgage on a newly built property. Older houses required borrowers to lay down larger deposits. House prices at this time were relatively stable and only rose each year gradually. However, when the demand for property started to exceed the supply, real estate prices grew. Also, many financial institutions began loosening their regulations, and many offered an array of mortgage products with less rigid rules. Borrowers could apply for 100% mortgages on new homes without putting down any deposit at all. People expected that house prices would continue to rise. Consequently, lenders considered offering these mortgages a minimal risk. The lure of large profits from mortgages took hold amongst the CEOs of the large banks. All of this large-scale unsecured lending created a housing bubble that would soon burst.

Bad Lending Decisions Led to the Banking Crisis

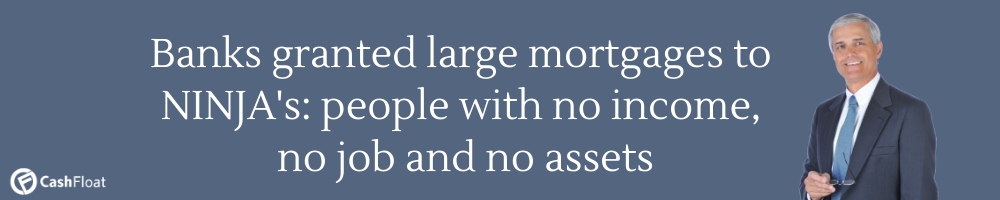

In the US, lenders offered subprime mortgages to consumers impolitely known as NINJAs. That is, No Income, No Job and no assets. In the UK these were euphemistically called ‘suicide loans’. Banks granted mortgages for 120% of the value of a house. Borrowers’ self-certification replaced proof of salary and financial credibility. Additionally, banks pressured their employees to sell more mortgages and related money products. Some financial advisors encouraged customers to inflate their salary on mortgage applications.

Lenders were lending too much money and then opting for securitisation. They would sell on the subprime debt to other banks and allow them to collect payments or repossess assets if the borrower defaulted. This erased the debt for the original lender, which allowed them to lend even more. Lenders based this continuous mortgage cycle on the delusion that house prices would continue to rise. Lenders assumed that once they sold the house, the debt to the bank was gone forever. Many new homeowners went straight into negative equity. The demand for property ownership was very high, and owners rightly imagined that their debt would quickly balance out when the value of their house grew.

Buy-to-Let

A new phenomenon was trending in the UK — many ordinary people were applying for buy-to-let mortgages. These mortgages allowed you to buy a second house and rent it out. Lenders promoted these mortgages on the premise that property values could only go up. Subsequently, the rent that owners would charge tenants would easily cover the mortgage payments. Many people entered the property market using the buy-to-let formula. They loved the idea that they could soon become millionaires (even if only on paper). They wouldn’t have to lay out any money since they could get mortgages for 100% value of the house.

Subprime Mortgages in the UK

Subprime mortgages are loans that granted to people with poor or even bad credit ratings. In return for the loan, the borrower pays a higher rate of interest. However, after a specified period, the rate should drop to the ‘normal’ interest rate. That is how it should have worked. But, the subprime mortgages were often sold on to a different bank without the knowledge of the borrower. Often, this meant a sudden hike in the interest rate from the new bank that had taken over the loan. Furthermore, there were no regulations in place to stop this process from happening more than once. Thus, a mortgage taken out with bank ‘A’ could end up with bank ‘D’ with frequent changes to the original contract for rates, terms and conditions.

Part of the problem in the UK was that banks and building societies had merged into large institutions. The only focus for these banks was high profits. Many of these large banks have CEOs’ with a background in other industries or retail sales but not in finance or banking. One of the most popular building societies in the UK was Northern Rock. The business sold over 200,000 subprime mortgages in the two years before April 2008 when the government nationalised the bank.

Banking Crisis – Central Bank Losses

Two other large banks, HBOS and RBS headed the lending spree during the early 2000s. HBOS was a company formed by the Halifax Building Society and the Bank Of Scotland. But, the roots of the former company lay in many other smaller building societies which had merged into one bank. At the time before the crisis, it was the fifth-largest bank in the UK. In 2003 an in-depth undercover sting by investigative reporters from a TV programme accused the bank of systematic fraud concerning mortgages. The programme uncovered that the bank advised borrowers to lie about their earning when completing self-certification forms for a home loan.

As early as 2004, people warned the directors of the bank about taking excessive risks. The subsequent Lloyds Bank takeover in September 2008 exposed the truth about the toxic loans. Lloyds posted a loss of £10 billion for HBOS in early 2009. Such was the far-reaching damage of the banking crisis.