When in debt, your prime concern will be keeping your home. Cashfloat will give you some tips on how to juggle debt management plans and your mortgage.

- It is unlikely for your home to be at risk if you pay your priority debts before your DMP payments

- It is usually worth waiting until a DMP is finished and your credit score has improved before applying for a mortgage

Cashfloat provides short term loans to help people overcome short term financial problems. As well as helping our customers overcome financial difficulty with our affordable loans, we publish helpful articles for people who are in debt distress. Our aim is to help as many people as possible.

In this article we will discuss whether or not your mortgage could be affected if you start a debt management plan.

Is My Home Safe When I Start a Debt Management Plan?

Debt can be a very difficult thing to face and it can cause people a lot of worry. One common worry is the extent to which it can threaten a person’s home. Many debt problems, in the UK, are solved by debt management plans. These are a commonly used informal debt solution, whereby someone who is in debt agrees to repay their debt, in full, at a slower rate than they originally agreed to. As an informal solution, debt management plans are not legally binding and there are no specific agreements made with your creditors regarding your assets while you are on one. This leaves many people worrying about whether their home is under threat.

Here we will try to explain how homeowners should approach a debt management plan and in what circumstances their home could be under threat. For more information about how debt management plans work, go to Chapter 3 of this guide.

Take Care of Your Priority Debts

When you begin a debt management plan (DMP), one of the first things that you should do is make sure that you are able to take care of your priority debts. Regular mortgage payments and mortgage arrears are priority debts and, instead of making mortgage payments in your DMP, you should budget yourself to make payments towards your mortgage before you make payments towards other debts which are covered by your DMP. As such, while you are on a debt management plan, you should make sure that you are able to keep up with your mortgage payments before you make payments to your other debts. You should not take money from your mortgage allowance, in your budget, to contribute to debts covered by your debt management plan.

Secured and Unsecured Debts

Debts which come in your debt management plan are normally unsecured debts. Unsecured debts are debts where none of your assets are used to secure the money you have borrowed. Secured debts, such as your mortgage, are debts where you use an asset of yours (your house in the case of a mortgage) to secure the money you have borrowed. Secured debts are always classed as priority debts.

If you fail to make payments towards secured debts, your creditors have the right to take control of any assets you used to secure the debt. In the case of unsecured loans, your creditors have to pursue legal action against you in order to take control of your assets, to pay your debts. If they choose to do so, only in rare cases will this be a threat to your home. As such, unsecured debts are much less of an immediate threat to your assets than secured debts. For that reason you should always pay your priority debts first. In the case of your mortgage, this will prevent any immediate threat to your home.

When Could Your Home Be At Risk While You are on a DMP?

The important point is that, for the majority of people, if they are able to agree to a debt management plan with their creditors and stick to making payments, their creditors will be unlikely to pursue any legal action against them. On top of this, when it does happen, it is only in rare cases that it threatens a person’s home.

The first stage of beginning a debt management plan is budgeting yourself. Your budget should allow you to cover your priority debts and provide a reasonable quality of life to you and your family before you make payments towards your DMP. As well as being able to pay your priority debts, it should be possible for you to meet your DMP payments. If the amount that you are able to offer your creditors is reasonable and you will be able to repay your debts quickly enough, most creditors will accept a debt management plan.

After creditors have accepted a debt management plan, they do still have the legal right to pursue court action against you, as a DMP is not a legally binding agreement. In theory, they could do this at any point. However, the vast majority of creditors would rather accept your DMP payments than pursue legal action against you to recover the debt. It is rare for this to happen. The time when this may happen is if you miss payments towards your DMP. Usually, you will need to miss several payments towards your DMP before a creditor will pursue legal action against you. That said, it is never a good idea to miss a payment and if you are struggling to make payments you should speak to your DMP provider at the earliest opportunity.

Communicate With Your Creditors

If you are struggling to make payments or if you think that you might miss one, you should speak to your debt management plan provider as soon as you can. They will be able to relay your situation to your creditors and try to negotiate a solution. Creditors are more likely to pursue legal action where there are missed payments without any communication from the debtor. Your DMP provider may be able to renegotiate payments to a more affordable level if you are struggling to keep up.

What If You Rent Your Home?

As with mortgage payments, your debt management plan should not affect a current tenancy agreement you have. When you budget yourself to make payments towards your DMP, you should make sure that you are able to cover your rent payments and any payments you need to make for rental arrears before you make payments towards your DMP.

Moving Into a New Rental Property

If you are looking to move into new rented accommodation you may find it more difficult to find a landlord who will accept you while you are on a debt management plan. While you are allowed to make a new tenancy agreement, prospective landlords may perform a credit check on you before allowing you to rent a property. While you are on a DMP, your credit score is likely to be low as you will be making reduced payments towards your debts. Your debts may also have a ‘payment arrangement’ note added to them allowing prospective landlords to see that you have had to make an arrangement with your creditors because you were unable to keep up with your debts.

Can You Take Out a Mortgage While You are on a Debt Management Plan?

If you are in a debt management plan and want to buy a home you may be wondering whether it is possible to take out a mortgage, while you are still paying off money with your DMP. This is particularly likely for people whose debt management plan has been running for some time and where they are able to meet their priority debts without too much difficulty. There is no regulation to prevent you from taking out a mortgage, however many people will find it more difficult to find a mortgage provider, while they are on a DMP, because of the effect it will have on their credit rating. While it is not impossible, fewer mortgage options are likely to be available and it will be likely that you will need to pay a larger deposit and a higher rate of interest.

While it may be more difficult, many people will still be keen to try. If you do want to try and take out a mortgage, you can speak to a mortgage advisor to find out what your options are. It is also a good idea to talk your situation through with your debt management plan provider to assess whether it is a viable option or not.

How do Mortgage Providers Decide If They Will Lend?

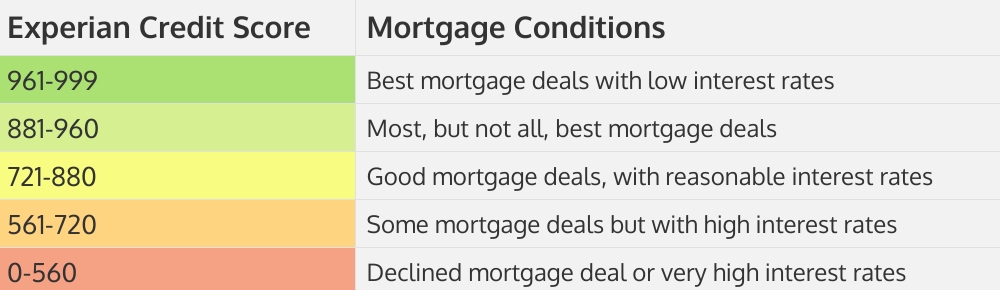

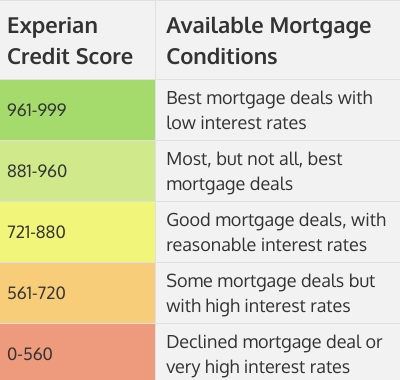

Mortgage providers lend large sums of money to people and, as a result, are quite particular about who they lend money to. Before they give someone a mortgage, they will want to know what the likelihood is of that person repaying the money. The less of a risk a borrower is seen to be, the more likely they are to get a mortgage. On top of this, more affluent and less risky borrowers are likely to get better mortgage deals.

Among the key things that mortgage providers look at, when assessing an application, are a borrower’s credit report and the amount of debt they have. Unfortunately for people who are on a debt management plan, they will have outstanding debt and their credit score is likely to be poor.

Your Credit Report

While being on a debt management plan will not be displayed explicitly in your credit report, your creditors may have added a ‘payment arrangement’ note to your debts. This is known as a ‘DMP flag’ and tells lenders that you have been unable to repay previous debts under the conditions that you agreed to when you first borrowed money. Mortgage lenders will see you as more of a risk as a result of this. On top of this, the reduced payments you will have made towards your debts will, most likely, have harmed your credit score directly.

While having a poor credit score does not prevent you from taking out a mortgage, it will limit your options and make it likely that you will need to pay a larger deposit and a higher rate of interest for mortgages which are available to you.

Mortgage Amounts, Deposits and Interest

As we just said, after lenders have assessed your mortgage application, they will decide whether or not they will lend you money and under what conditions. If lenders will provide you with a mortgage, while you are on a debt management plan, it is likely that they will offer you a smaller mortgage. On top of this, they will also be likely to ask for a larger deposit and charge a higher rate of interest. This means that, while it is not always impossible to take out a mortgage while you are on a DMP, many people find that the deposit requirements and interest rates make them unaffordable or impossible to start.

Wait Until Your Credit Score Improves

Before looking into getting a mortgage to buy your own home it is often a better plan to completely clear your debts and to wait until your credit score improves. After you have cleared yourself of outstanding debts and your credit score has improved, mortgage providers will be far more likely to offer you favourable mortgage conditions. Your credit score is always likely to be poor while you are on a debt management plan and the best time to improve it is after you have finished it.

How To Improve Your Credit Score

After you have finished your debt management plan there are some simple ways you can improve your credit score:

- Check your credit report. By checking your credit report you will be able to correct any errors or misinformation which could be damaging your score.

- Register on the electoral roll. Being registered on the electoral roll helps lenders to verify your personal information and improves your credit score.

- Pay your bills on time! This is the most important thing. Make sure that you pay all of your bills on time in future. The longer you keep on top of your credit, the better your credit score will become.

Other Difficulties While on a Debt Management Plan

As well as it being difficult to get mortgages while you are on a debt management plan, other forms of credit will be harder to obtain as well. Like mortgage providers, other prospective lenders will also look at your credit score when they decide whether or not to lend you money. It will be hard to obtain other forms of credit and in many cases it will be impossible. On top of this, it is also usually not advisable to take out new credit while you are on a DMP. Cashfloat recommends that you do not attempt to borrow payday loans or small personal loans while you are on a debt management plan.

In Summary…

The important thing, if you are on a debt management plan, is to stick to making the payments that you have agreed to make. It is when people fail or are unable to make payments that problems occur. If you are struggling to make payments or if you think that you might miss one, you should speak to your debt management plan provider at the earliest opportunity and open up communications with your creditors in order to resolve the problem.

For people who are looking to take out a mortgage while they are on a debt management plan, this is possible. However, it will be difficult and it is often better to wait until a debt management plan has finished and your credit score has improved before you start looking into mortgage options.

Next up in this guide to debt management plans is an explanation of what happens to the interest charges on debts you are paying off with a debt management plan.

Chapter 9:

Will a Debt Management Plan Affect My Partner?

Chapter 11:

Can You Get a New Mortgage With a Debt Management Plan?