How does an IVA and debt management plan differ? Cashfloat will clarify this and help you to decide which one suits your circumstances better.

- Debt charities provide free, professional debt advice

- IVAs clear your debt quicker than debt management plans but they also have a greater negative impact on your credit score

Western Circle, trading as Cashfloat, offers payday loans across the UK. We have already helped thousands of UK citizens overcome short term money problems with our payday loans and financial advice.

In our guide to debt management plans, we aim to help anyone struggling with debt by explaining how debt management plans work. In this article, we will discuss the differences between two common debt solutions: debt management plans (DMPs) and individual voluntary arrangements (IVAs). We will explain how they both work and why you would choose one over the other.

Debt Management Plan Vs an Individual Voluntary Arrangement (IVA)

Stress and worry can impair your judgement and make it hard to find the right solution to debt. Also, many people are not familiar with the ways in which debt can be tackled. The more good advice and information you receive, the better. This article will provide a good basic introduction to debt management plans and IVAs and should help to give you an indication of which one is better for you.

Always Seek Professional and Impartial Debt Advice

If you are coming to terms with the fact that you are struggling to repay your debts and are looking for a solution, it is important that you make the right choice about how to tackle the problem. There are many debt solutions available. Debt management plans and individual voluntary arrangements are just two of many. You should always seek professional and impartial advice before you make a choice about how to tackle a debt problem.

Luckily, for people who are in debt, free debt support is widely available. There are now many charitable organisations, such as StepChange and National Debtline, who offer free, professional and impartial advice to people who are in debt. As well as offering advice about how to approach debt, many of these charities also support people the whole way through their recovery from debt.

In the stressful situation of being in debt, you may be tempted to approach debt management companies that you see in TV adverts. However, it is important to be wary of debt management companies. We always recommend that people seek advice from charitable organisations instead.

Payplan is one of the popular debt charities that can guide you to a debt solution. They have helped many people in the UK. Denise is one such customer; Payplan helped her to clear her debt by helping her to set up an IVA. Here is her story:

Avoid Debt Management Companies

The difference between debt management companies and debt charities is simple. Debt management companies are businesses which charge fees, whereas, charities do not charge a fee and act, simply, in the best interest of their clients. Often debt management companies promise free advice and even free support throughout debt recovery. However, it is often the case that they really charge fees to their customers at a time when they can least afford them and, also, when the same support is available for free from a charitable organisation.

Here’s a brief explanation of how debt management plans and individual voluntary arrangements work.

How Does A Debt Management Plan Work?

Debt management plans are an informal agreement made between a debtor (someone who owes money) and their creditors (people they owe money to). Under a DMP the debtor will agree to pay back, in full, what they owe to their creditors at a slower rate than what they originally agreed to. As part of a DMP, the debtor will, normally, also ask their creditors to freeze interest and other charges on the debt. This is to prevent the debt from increasing, making it more difficult to repay. There are no eligibility criteria for beginning a debt management plan, as there are with many other debt solutions.

Debt management plans do not allow you to ‘wipe’ your debts without paying them off. Under a DMP, although you may avoid interest and charges, you will have to fully repay your debts.

DMPs are suitable for people who have enough money to spare to repay their debts, but can’t afford to stick to the repayment conditions they originally agreed to when they borrowed money. As an informal agreement, they are not legally binding and depend on the participation of both parties to be successful. This makes it possible for creditors to cancel your DMP and this is a concern for many people. In reality, as long as a debtor sticks to making the repayments that they agreed to, few creditors back out of a DMP after they have agreed to start one.

Most DMPs are arranged by a third party who acts as an intermediary between a debtor and their creditors. Debt management plans are not specifically noted in your credit report. However, being on one will still affect your credit rating. This is because you will be making reduced payments towards your debts. On top of this, your debts may be noted as having ‘payment arrangements’ in your credit file. Debt management plans allow people to clear their debts at an affordable rate, while avoiding insolvency and other consequences that come with other debt solutions.

How Does an Individual Voluntary Arrangement (IVA) Work?

An IVA is often used as an alternative to going bankrupt. IVAs are a formal (legally binding) agreement made between a debtor and their creditors. Under the agreement, a debtor will agree to make affordable payments towards their debts for a period of 5 to 6 years. After this period, their outstanding debts will be wiped. As they are a form of insolvency, IVAs are managed by an insolvency practitioner.

In order to start an IVA you have to offer payment amounts, that you can afford, to your creditors. They will then vote on whether or not to accept your offer. If they do accept it, your IVA will begin. After it has begun, it is a legally binding agreement and both you and your creditors will have to stick to it. After an IVA has begun it will also be shown on your credit report and this can have serious consequences. While they are not as serious as bankruptcy, having an IVA can severely limit people’s financial options.

As soon as an IVA is agreed, interest and additional charges on debts are stopped. This is one of the major attractions for people of an IVA, as it prevents ‘persistent debt’ where people are unable to keep up with their debts because of interest rates and charges. In addition to this, your creditors will no longer be able to contact you and will have to carry out all communication with your insolvency practitioner instead.

You will have to meet the conditions of the IVA for as long as it lasts and, after it has finished, your outstanding debts will be wiped. As part of entering an IVA agreement, if you are a homeowner, you may be required to release equity from your house to contribute towards your debts. Additionally, you may be required to take out a loan which is secured against your property to contribute towards your debts. This means that IVAs can have serious consequences for homeowners.

IVAs are not available in Scotland. In Scotland, protected trust deeds are available instead. These offer a similar solution, although there are different benefits, risks and fees associated with them.

You can find out more about how to set up an IVA, on the UK Government’s website.

Comparing Debt Management Plans (DMP) and Individual Voluntary Arrangements (IVA)

While debt management plans and IVAs are similar on the face of it, they do have key differences and one solution will always be better than the other, depending on the situation. The key differences between them are that IVAs are legally binding, whereas DMPs are not. Also, DMPs require you to repay your debts in full, whereas with an IVA any outstanding debts you have, after it has finished, will be wiped. Remember to seek professional and impartial advice before deciding whether a DMP or an IVA is right for you.

How Long Will it Take to Clear Your Debts?

Under an IVA, you will repay your debts over a fixed period of time. Usually this is five years. However, some IVAs last for six years and they can be extended for even longer if you miss payments. After your IVA has finished, your outstanding debts will be wiped and you will no longer be in debt to your creditors. Debt management plans have no fixed length of time. How long it takes to finish a DMP will depend on how much money you have available and how much you owe. If you have a large amount of debt and little money to repay it, then being on a debt management plan could last longer than an IVA. However, if you have a relatively small amount of debt and can repay it quickly enough, a DMP could be quicker than an IVA.

How Will Your Credit Rating be Affected?

Both DMPs and IVAs will negatively affect your credit rating. An IVA is a form of insolvency and it will immediately be recorded on your credit report, once it has been agreed. It will stay on there for six years. During this time, you will find it very difficult to get credit and you will even have to get permission from your insolvency practitioner if you want to take out more than £500 in credit. Beginning an IVA has immediate and serious consequences for your credit score.

While debt management plans are not specifically recorded in your credit report, they will still have an effect on your credit score. Under a DMP you will be making reduced or ‘partial’ payments towards your debts and this will be recorded. Also, your creditors may note the plan you have made with them as a ‘payment arrangement’ for the money that you owe them. This will be likely to have an impact on your credit score.

The effect to which an IVA or a DMP will affect your credit score will depend on your circumstances and one may be a better choice than the other when it comes to limiting the damage to your credit score. You should speak to an impartial debt advisor to get a clearer picture of how much your credit score will be affected by each choice.

What are the Costs?

Remember that if you choose a debt management company to administer either of these agreements it will cost you extra money in fees to the company. It is always better to go with a free debt charity, such as StepChange or Christians Against Poverty.

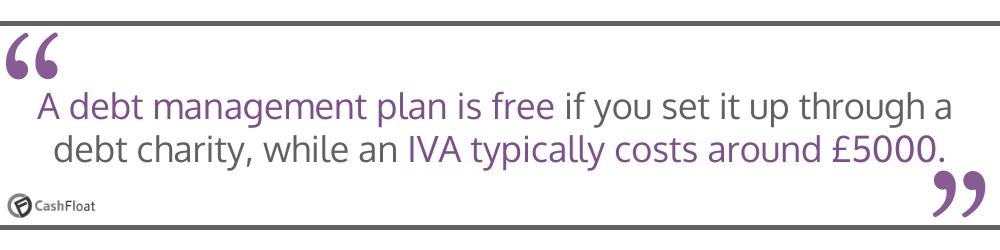

If you have a debt management plan arranged for you by a free, charitable organisation it will cost you nothing in fees. All of your money will go towards repaying your debts. As such, there are no costs to making a debt management plan. IVAs, on the other hand, do have associated fees and costs. Typically, it costs around £5000 to have an IVA. These fees go towards paying the insolvency practitioner, who oversees your IVA.

What Happens to Interest on Debts?

Under an IVA, as soon as it has been agreed, interest charges and additional fees for your debts cannot be added by your creditors. This means that your debt is guaranteed not to rise during the time that your IVA is in place. As soon as an IVA is in place the problem of increasing, persistent debts, that happens as interest and charges add up, goes away and you will be able to make regular payments towards your debts.

While the same is possible (and normally happens) with a debt management plan, it is not guaranteed. This is because they are an informal debt solution. Your creditors are not obliged to freeze interest and fees and, even if they do initially agree to do so, they can change their minds at any time. This means that it is possible that additions will be made to your debts while you are paying them off. In practice, many people find that if they are able to successfully negotiate a DMP with their creditors, then they will agree to freeze interest charges and fees while it is in place.

Are Agreements Legally Binding?

One of the main differences between an IVA and a DMP is that IVAs are legally binding. This means that, once it is in place, neither you or your creditors can back out of it.

For an IVA to begin and for it to become legally binding it must be agreed to by the creditors to which you owe at least 75% of your debts. For example, if you have four creditors and you owe an equal amount to each one, then three of them must agree to your proposal. After they have agreed, it will become legally binding for all of your creditors. This has both positives and negatives. On the plus side, they will all be obliged to freeze your interest and charges, they will have to cease pursuing you for the money and they will have to accept the payments that you make to them. However, this also means that you have to keep to the payments that you agreed to make. If you fail to make your IVA payments, you will be back at the start and will, potentially, have wasted time making those payments. There are a considerable number of people who fail to keep up with IVA payments and it is worth considering the fact that it may be difficult to do so.

A debt management plan is an informal debt solution and there is no obligation for all your creditors to take part. Similarly, if you find that you are unable to keep to the agreement, then you can back out at any time. The option of leaving a DMP may be appealing. However, this also means that your creditors are also able to cancel the agreement at any time. Theoretically, at any time, they could reject the plan and take action against you to reclaim their money. Alternatively, they could decide to continue adding interest and charges while you are trying to repay your debts.

Will it Affect My Employment?

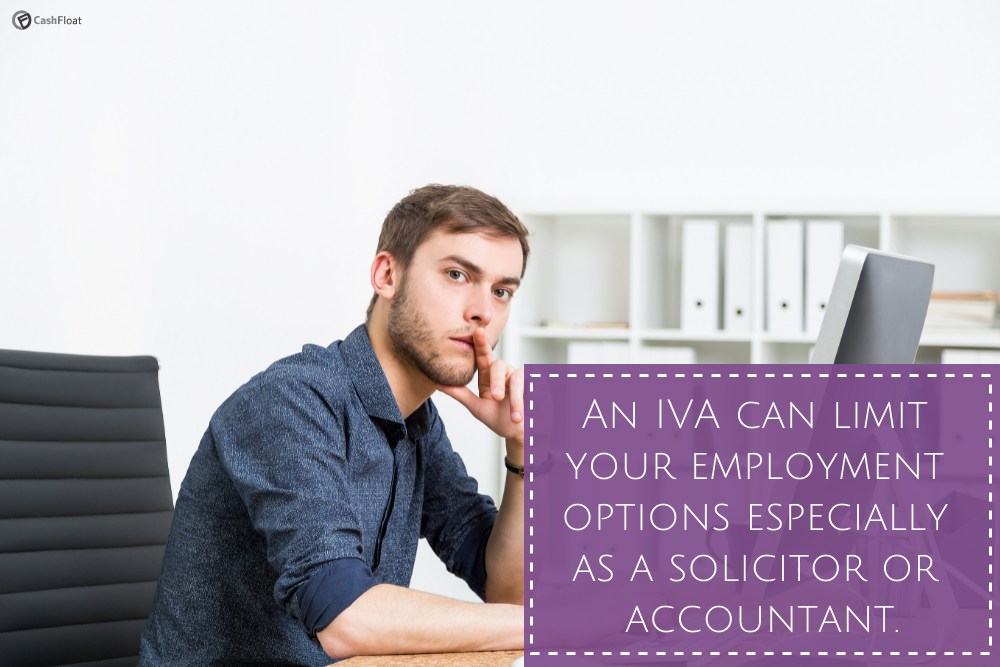

Someone’s ability to work in certain professions, such as as a solicitor or as an accountant, may be affected by insolvency. As a form of insolvency, while it is not as serious as bankruptcy, having an IVA may affect your employment. If you are considering taking out an IVA, it is worth speaking to a debt advisor to see if your employment will be affected by it. Taking out a debt management plan does not usually have an effect on your employment status.

In Summary…

If you are deciding whether a debt management plan or an individual voluntary arrangement is the right solution to your debts, then it is a good idea to seek impartial and professional advice before you make a choice. While this article should have helped you to understand the main differences between these two debt solutions, the best choice for you will depend on your circumstances.

The best people to go to for advice are charitable organisations which provide free debt advice, such as StepChange and National Debtline. Companies which make a charge for providing this type of service may give you biased advice which is designed to generate them the most money in fees.

Read the rest of this guide to debt management plans to find out everything you need to know about how they work and where the best places are to go to get one.

Chapter 5:

Can I Manage My Own Debt Management Plan?

Chapter 7:

Debt Management Plan Vs Debt Relief Order