Struggling to pay your housing costs? You may be eligible for help. Read this article from Cashfloat to find out all about housing benefits.

- At the end of 2020, almost 3 million people still received Housing Benefit, at an average of £108 per week.

- If you need help with the cost of housing, but aren’t eligible to claim Housing Benefit, you will have to apply for Universal Credit instead.

In this chapter, we will be looking at how housing benefits can help people to pay their different housing costs. We will cover rent, paying a mortgage, living in shared ownership schemes or living in temporary, supported or sheltered housing.

In 1982 local councils introduced the Housing Benefit to provide support for those who needed help paying their housing costs. Universal Credit is currently replacing Housing Benefit.

This chapter discusses how Housing Benefit works, who can still make a claim for it and how the Universal Credit housing element differs. Additionally, we will explain how those receiving Housing Benefit will move over to Universal Credit.

Housing Benefit and Universal Credit

Help is available to pay your rent if you are on a low income or completely out of work. Depending on your circumstances, you might be able to receive all, or part, of your rent, mortgage or other costs.

Traditionally, local councils provided help through Housing Benefit and until recently, people who needed help to pay their housing costs would apply for this. However, Universal Credit is now replacing Housing Benefit. This means that most new claimants for housing support will have to apply for Universal Credit instead. While this is the case, many people still receive Housing Benefit and some people can make a new claim for it.

The amount that people receive for Housing Benefit or Universal Credit is individual. What you receive will depend largely on your circumstances, where you live and what payments you need to cover. You will usually receive a monthly payment.

In this article, we’ll explain everything that people need to know about getting help to pay for housing. We’ll explain how to apply for housing support under Universal Credit, who can still apply for Housing Benefit and what people who are currently receiving Housing Benefit should expect in future.

Should I apply for Universal Credit or Housing Benefit?

This is the first question that most people ask. Nowadays, most new claimants for financial support to cover the cost of their housing should apply for Universal Credit. Housing Benefit is now only available to new applicants who are over the state pension age or live in sheltered, supported or temporary housing. For a full explanation of the eligibility rules for Housing Benefit, go to the gov.uk website here.

Who is Eligible for Housing Support Under Universal Credit?

There is no set level of income to be eligible for Universal Credit. What you you can receive depends on your circumstances. Generally, people who are on a low income or are unemployed can make a claim. Therefore, if you struggle to pay for your housing cost, it is worth seeing if you are could get help under Universal Credit. The quickest way you can find out what you might receive is to use a benefits calculator.

To be eligible for support under Universal Credit you must:

- Be over 18 years old (with a few exceptions for 16-17 year olds).

- Be under the state pension age.

- Live in the UK.

- Have less than £16,000 in savings as an individual if you make an individual application or as a couple if you live with your partner.

How the Universal Credit Housing Element Works

Everyone eligible for Universal Credit is allocated a maximum standard monthly allowance, which is calculated according to their age and whether they live with a partner. From the maximum standard allowance, deductions are made according to a person’s circumstances. Following these deductions, a person’s individual standard monthly allowance is calculated. This amount is provided to cover a person’s general living expenses.

On top of a person’s standard monthly allowance, they may be eligible for extra payments if they have extra costs to cover. The cost of housing may be one of these extra costs. If the government approve you for extra help to cover the cost of housing, you will receive a payment for this on top of your standard monthly allowance.

Standard Maximum Monthly Allowances | |

|---|---|

| Personal Circumstances | Maximum Monthly Amount |

| An individual under 25 | £311.68 |

| An individual over 25 | £393.45 |

| A couple both under 25 | £489.23 (for both people) |

| A couple with at least 1 over the age of 25 | £617.60 (for both people) |

Many people will receive less than the standard maximum monthly allowance. People who live with their partner will have to make a joint application and usually receive less per person than an individual claimant. When you make a joint application, both you and your partner’s earnings and savings will affect the outcome.

Extra Payments for Housing

If you qualify for extra payments to cover your housing cost, you will receive these payments on top of your standard monthly allowance. This is known as receiving the ‘housing element’ of Universal Credit. How much you receive depends on your circumstances, such as where you live, whether you rent or own your home and whether or not you have any income. The quickest way to find out what you could receive is to use a benefits calculator.

Different support is available for people according to whether they pay a mortgage, live in a shared ownership scheme or pay rent.

It is important to note that while Universal Credit does provide support to people who need to make mortgage payments, there is a 9 month qualifying period from the date of their first claim to when they can receive any payments. During this qualifying period, the person must have no earned income and no breaks in their Universal Credit claim. People who were receiving Jobseeker’s Allowance or Employment and Support Allowance before their claim for Universal Credit can use the time they were claiming this to contribute towards the qualifying period.

Any help that you receive after this period will be in the form of a loan, on which you will be charged interest, and which you will have to pay back when you sell the property or transfer it to someone else. The amount that people can receive depends on their circumstances. You can use a benefits calculator to see how much you could receive.

People who need help to cover the costs of privately paid rent do not need to wait for any qualifying period. That said, there can be delays before you receive your first payment and so it’s always worth telling your landlord that you are claiming Universal Credit. Your Local Housing Allowance Rate determines how much you can receive. These rates are set to be the same as other people who live in your area and have a property with the same number of bedrooms as you. You can check the Local Housing Allowance Rate in your area here.

Most people who live in shared accommodation and, also, anyone who is single and under the age of 35 will receive the shared accommodation rate of Local Housing Allowance. You can find out your local shared accommodation rate here.

People who rent from their local authority, local council or from a housing association will normally receive their full rent as part of their Universal Credit Payment. If you have any spare bedrooms in your house, the amount that you can receive will be reduced. If you have 1 spare bedroom it will decrease by 14% and if you have 2 or more, it will decrease by 25%.

Living in a shared ownership scheme normally means that people pay rent for the share of their home that they do not own and a mortgage for the share that they do own. The rental proportion is normally paid to housing associations who provide the shared ownership scheme.

Payments for the rental proportion of a person’s housing costs are received as part of their Universal Credit payment, in the same way that people who just rent from a housing association receive them. Payments for the mortgage part of costs associated with shared ownership schemes are more complicated. You will need to speak to Jobcentre Plus when you make your claim and see if you can receive any support. If you are eligible, there may be a waiting period before you can receive any payments. If there are service charges associated with your shared ownership schemes, you may be able to have these covered under Universal Credit payments, or under other benefits.

The Benefit Cap

While it is possible to have all of your housing costs covered by Universal Credit, some people will find that the total amount that they can receive in benefits is affected by the benefit cap. The benefit cap applies to Universal Credit and extra payments received under it for housing. Under the cap, there is a limit on the total amount of benefits a person can receive.

Some people, notably those who suffer from a disability or receive Carer’s Allowance, are exempt from the cap. Also, for most people, there is a grace period of nine months after first claiming Universal Credit in which it does not apply.

However, the cap will affect many people. Here’s how much the cap is set at:

| Inside Greater London per week / per year | Outside Greater London per week / per year | |

|---|---|---|

| For a single adult | £326.29 / £16,967.04 | £283.71 / £14,753.04 |

| For a single parent whose children live with them | £486.98 / £25,323 | £423.46 / £22,020 |

| For a couple | £486.98 / £25,323 | £423.46 / £22,020 |

Find out more about the benefit cap here.

How to Apply for Housing Benefit under Universal Credit

If you are unsure whether you are entitled to help under Universal Credit, it is always good to use a benefits calculator to what you could receive. You can apply online, and you will need to provide personal information. This includes information about your income, details of any savings you have and details of the current cost of your housing. If you need help with your application, ring the Universal Credit helpline on 0800 328 5644.

Remember that if you live with your partner, you will need to make a joint claim. You will normally have to make a joint claim if:

- You are married

- In a civil partnership and live together

- You are unmarried but live together as if you are a married couple

Generally, if your partner is a regular visitor to your home but owns or rents a property elsewhere, this will not count as living together. Also, if you still live in the same household as your previous partner, but you are no longer a couple, this will not require a joint application.

It will take around five weeks from application until you receive your first Universal Credit payment. If you need the money before that, apply for a payment advance here. If the money hasn’t come through and you need money in an emergency, you could apply for a loans for unemployed people online. As these loans are expensive, make sure you will have the money to pay it back on time.

Housing Benefits Change of Circumstances

After your claim for Universal Credit is accepted, you will continue to receive regular payments until either your circumstances change and you become eligible for more benefits, or until you begin to earn money. As you earn more money, the amount that you receive will decrease. For every £1 you earn, your Universal Credit payment will drop by 63p until you reach your personal limit. Your limit varies according to your circumstances. After you reach your limit, your Universal Credit payments will stop.

The Work Allowance for People with Children

People who have children are given a ‘work allowance’ under Universal Credit. This is an amount that they are allowed to earn before their Universal Credit payment will decrease. People who receive support for their housing costs have a reduced work allowance. For people who receive no support for their housing costs, the work allowance is £673 per month. For people who receive support for the cost of their housing, it is £404 per month.

What Happens to Other Benefits When you Claim Universal Credit

If you are already claiming other benefits and need to make a new claim for Universal Credit to cover your housing costs, your other benefits may be affected. Normally, payments you receive for Housing Benefit, income-related Employment and Support Allowance, income-based Jobseeker’s Allowance, Child Tax Credits, Working Tax Credits and Income support will end when you start a new claim for Universal Credit. While you will still receive support under Universal Credit, the amount that you receive may be different. You can use a benefits calculator to determine if you would be better or worse off under Universal Credit.

Note: Don’t forget that you may also be entitled to Discretionary Housing Payment if you need additional help on top of what you can receive under Universal Credit. Go to the end of this chapter to find out more.

Housing Benefit Application

Most people making new claims for support with housing costs, will now have to apply for Universal Credit. However there are some people still eligible for the legacy housing benefit, and they can still make a claim. Below are eligibility requirements:

If you are over the state pension age, to be eligible for Housing Benefit you must be one or more of the following:

If you are under the state pension age, to be eligible for Housing Benefit you must be one or more of the following:

In addition to meeting the above requirements, several things may make you ineligible for Housing Benefit. Among other things, you will be ineligible if you are paying a mortgage on your own home, if you have over £16,000 in savings, if you live with a close relative or if your partner already claims Housing Benefit.

What People Can Receive

You can receive Housing Benefit to pay for privately rented housing, or housing that you rent from a local authority or a housing association. Unlike Universal Credit, there is no support for people who own their own home and need to make mortgage payments. However, these people may be able to claim Support for Mortgage Interest.

Suppose you are eligible for Housing Benefit and you live in privately rented accommodation. In that case, you will be able to claim up to a maximum of either your Local Housing Allowance rate or your actual rental amount, whichever is lower.You can find out your Local Housing Allowance rate here.

The total amount you will receive depends on your personal circumstances and any income, pension or savings you have. People do not usually find out exactly how much they will receive until after they make a claim. You can use a benefits calculator to see how much you could receive.

People who rent from their local authority or a housing association will be able to claim up to the total cost of their housing, plus any service charges they have to pay. Service charges include mandatory charges that you have to pay as part of your rental agreement, such as lift servicing or grounds maintenance. It does not include things like utility bills.

The actual amount that people receive depends on their personal circumstances. It takes into account any income, pension or savings they have and whether or not they have any spare bedrooms in their home. If a person has 1 spare bedroom in their home, their Housing Benefit will decrease by 14% and if they have 2 or more spare bedrooms, it will drop by 25%. Note that all adult couples, 2 same-sex children under the age of 16 and 2 children of different sexes under the age of 10 are expected to share a bedroom. Rooms used by foster carers or students, or members of the armed forces who are temporarily absent from their home, do not count as spare bedrooms.

How the Benefit Cap will Affect your Claim

As with housing support provided by Universal Credit, payments made under Housing Benefit may be affected by the benefit cap. Under the benefit cap, the total amount of benefits that a person, or a couple, can receive is limited. For a couple outside of Greater London, the maximum amount they can receive is usually £20,020. Inside Greater London, it is £25,323. Find out more about the benefit cap here.

Note: Don’t forget that you may also be entitled to Discretionary Housing Payment if you need additional help on top of what you can receive under Housing Benefit. Go to the end of this chapter to find out more.

Information for People Who Already Receive Housing Benefit

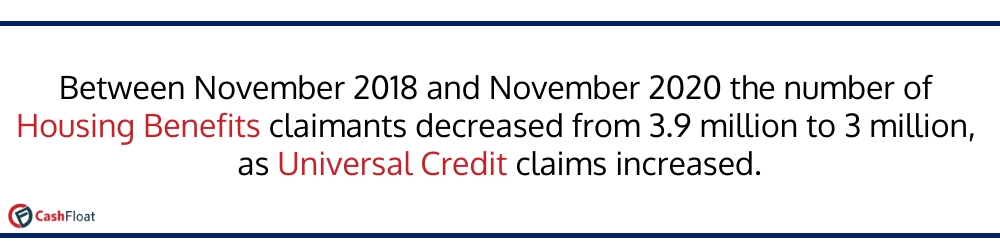

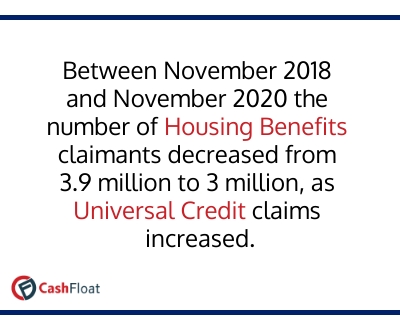

Housing Benefit is now one of the legacy benefits, which Universal Credit is replacing. However, as of August 2022, there were 2,534,000 people still receiving Housing Benefit, at an average of £135.95 per week. The government plans to move everyone eligible to receive Universal Credit over to it by the end of 2024. In the meantime, many people who receive Housing Benefit but are eligible for Universal Credit can stay on Housing Benefit.

When will People Move Over to Universal Credit?

As of early 2021, people are only moving over to Universal Credit, from legacy benefits such as Housing Benefit, in what is called ‘natural migration’. This means that people are moving over voluntarily for one of the following reasons:

- They need to make a new claim for Universal Credit because they have become entitled to another benefit covered by it.

- They choose to move over to Universal Credit, as they will be better off on it.

- Their current claim for a legacy benefit ends, then they will be unable to renew their claim but will have to apply for Universal Credit instead next time they make a claim.

The government plans to move everyone over from legacy benefits to Universal Credit by the end of 2024 and eventually they will introduce ‘managed migration’. Under managed migration, the government will write to people and request that they apply for Universal Credit and end their current claims to any legacy benefits they receive.

Will I Receive More or Less Under Universal Credit

Whether a person will receive more or less under Universal Credit depends on their circumstances. Use a benefits calculator to see how much you will receive under Universal Credit. You may find that you will be better off under Universal Credit.

Note: Don’t forget that you may also be entitled to Discretionary Housing Payment if you need additional help on top of what you can receive under Housing Benefit. Read on to find out more.

Extra Housing Support: Discretionary Housing Payment, Extended Payment of Housing Benefit and Council Tax Reduction

On top of the normal help that is available through Universal Credit and Housing Benefit, other support is available. If your payments do not cover what you owe, you may be able to claim Discretionary Housing Payment. If you are claiming Housing Benefit and will struggle to pay your rent when you return to work, you may be able to claim an extended Housing Benefit payment to tide you over while you return to work. In addition to this, many people who are eligible for Housing Benefit or Universal Credit will become eligible for Council Tax Reduction.

If your Housing Benefit or Universal Credit payment is not enough to pay for a roof above your head, you may be able to claim Discretionary Housing Payment. You should not need to take short term finance loans so that you can pay your rent.

Many more people have received the Discretionary Housing Payment since the removal of the spare room subsidy, otherwise known as the bedroom tax. Under this scheme you are able to appeal to your local authority for extra support. If you find that what you receive under either Housing Benefit or Universal Credit is not enough to cover the cost of your housing, check if you are eligible for Discretionary Housing Payment.

There are various situations in which your local authority might decide that you should receive a payment. Examples include, if your Local Housing Allowance rate is lower than what you actually pay or if your benefits are reduced because of the benefit cap.

You can also claim Discretionary Housing Payment to cover one-off expenses, such as deposits to secure a property, rent advances or the costs of moving house.

It is possible that your claim for Housing Benefit will stop when you return to work. If this means that you will be unable to pay your rent while you begin working again, you might be eligible for an extra four weeks of Housing Benefit. This is called ‘Extended Payment of Housing Benefit.’

Normally, you do not have to make a claim and your council will contact you to tell you that you are eligible. Generally, to be eligible, you must have been receiving certain benefits continuously for at least 26 weeks up to the time when you started work.

Many people who become eligible for Housing Benefit or Universal Credit will become eligible for a reduction in their council tax. You should contact your local council and see if you can have your council tax rate reduced as well.

If I have a child studying away from home as a full-time student, does his room count as a spare bedroom?

No. If your child is a full-time student or in the Armed Forces, their bedroom does not count as a spare bedroom.

Can I receive Housing Benefit or Universal Credit for a room in a flatshare?Yes, you can claim for a bed-sit or a single room in shared accommodation. You will receive the Shared Accommodation Rate of either Housing Benefit or Universal Credit. Single people under 35 can only claim the shared accommodation rate, whether they live in shared accommodation or not.

Can I claim Housing Benefit or Universal Credit if I am a full-time student?Full-time students are not eligible for Housing Benefit unless they:

- are disabled.

- have a child.

- live with their partner and they are eligible for Universal Credit.

- are under 21 and have no parental support.

Your monthly Universal Credit payment includes a housing benefit so you can pay your landlord directly.

When will I have to move from Housing Benefit to Universal Credit?The government plans to move everyone over by 2024.

Should I apply for Housing Benefit or Universal Credit?Universal Credit is replacing Housing Benefit. Apply for Universal Credit unless you are over the state pension age or live in sheltered, supported or temporary accommodation.

Summary: Housing Benefits UK

This article mainly discussed Housing Benefit and Universal Credit for those who need support for their housing payments. If you are on a low income or unemployed, you should see if you are eligible to receive either of these benefits. Don’t forget that there are more benefits that you can get for housing costs if these are not enough. These include Discretionary Housing Payment, Extended Payment of Housing Benefit and Council Tax Reduction. On top of this, you may be able to receive benefits that aren’t related to your housing. Have a look at the rest of our guide to see what else you might be entitled to.