Which credit card should you get? This handy guide from Cashfloat explains what to look for when you compare credit cards, so you make the best choice.

- Don’t just go for the first credit card offer you see

- Sending off multiple applications can damage your credit history

- Introductory offers sound great – but remember, they will run out

In spite of warnings from Shakespeare that we should ‘neither a borrower nor a lender be’, most people now use some form of credit in their daily lives. As long as you use a card sensibly and heed the warnings about overspending, then making a purchase using a card can be beneficial. This is especially true if the alternative would be an instant loan online. For example, making a payment for a holiday using a credit card can give you extra insurance protection.

In this chapter, we will take a close look at the factors to consider when choosing a credit card.

How to Compare Credit Cards

Although it can be tedious, doing some research into credit card offers can help you make the right choice for your individual circumstances. There are a myriad of money comparison websites where you can compare credit card offers, as well as individual card provider websites where card companies advertise their particular credit cards.

Be aware that the interest rates offered by card providers can change very quickly as companies compete with each other to make the best offer. What you see advertised one day may be different a few days later.

If you’ve read Chapter 6 of this guide, you will be aware of the different types of credit card. Certain types of credit card suit certain users better than others. While the types vary, the key things to look at remain the same and here’s what you should look for when you’re comparing credit cards.

Annual Percentage Rate (APR)

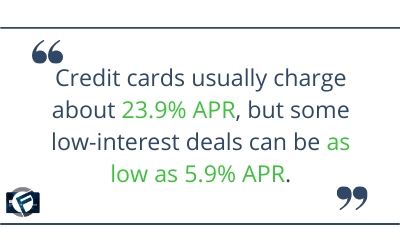

For most people, the first thing to look for when comparing credit cards is the APR. All card companies must quote the Annual Percentage Rate (APR) of any credit cards that they offer and this figure gives a good baseline indication of how much it will cost you to borrow money with a credit card.

The APR indicates the cost of borrowing over one year. If, for example, you borrow £500 with an APR of 20% for one year, this will cost you £100. However, the speed at which you pay money back will affect how much you pay and the terms and conditions of your contract will also affect how much you pay. It is important to check the terms and conditions of a credit card agreement carefully before you take on an offer.

APR is only an indicative figure. The advertised APR only has to actually be given to a certain percentage of customers, so you may not get the interest rate that is advertised. You should check that the APR you are actually offered, after you apply, matches the advertised APR. Additionally, the advertised rate will normally only apply to purchases and not to cash withdrawals. Balance transfers may also incur extra fees. The APR also only includes compulsory charges for borrowing and doesn’t include fines, additional fees or optional extras, such as payment protection. On top of this, rules about payment dates may complicate things further and APRs also come as fixed and variable rates.

For these reasons, while APR is usually the best way to compare credit cards, it is always good to check the smallprint and not just base your decision on a quick assessment of the APR.

Introductory Interest Rates

Many companies will tempt new customers with an introductory offer of 0% interest rates for a fixed period of time. As long as you know that you can pay off the balance before the introductory period is over, a good way to fund a large purchase is by taking out one of these cards, and many people do this. However, these are also a good option if you just want a credit card for general spending, because you will have a lengthy period of time before you start to pay any interest.

If you want to transfer a balance from another credit card to one with 0% interest, always take into account that a fee will often be charged. This is often charged as a percentage of the amount being moved across. For balance transfers, balance transfer cards are often the best.

Reward Schemes

Tempting as they may seem, some of the rewards and benefits on offer from card companies are not always a good deal. You might be offered cashback, travel insurance, air miles or access to airport lounges. These cards often come with an annual membership fee and other costs. Unless you will make good use of rewards, throughout the year, the annual fee may not be worthwhile. Cashback credit cards often come with extra hidden costs.

Although some people might find rewards useful, for most people who will rarely use them, they are fringe benefits that do not outweigh the cost.

Additional Charges And Fees

One of the contract terms that you should subject to most scrutiny, when you compare credit cards, is the summary of fees and charges. Credit card agreements can be complicated and there are a number of additional charges and fees that credit card providers can charge their customers. Always take a good look at the terms and conditions and know what you are letting yourself in for. Several extra fees to look out for are:

- Fees for late payments. There are now limits to how much card companies can charge for this. It is usually £12. Incidentally, the fee for a late repayment when it comes to UK payday loans is £15.

- Cash withdrawals made with credit cards will usually attract a fee of around 3% of the amount being withdrawn and you will usually pay a higher rate of interest for this kind of transaction.

- Some companies make charges for using a card while abroad.

- Finally, be careful to look at what fee will be charged should you inadvertently go over your credit limit.

The fees and charges which credit card companies charge to their customers vary a lot and it is important that you read your individual contract and be sure of exactly what you will have to pay.

Credit Limit

The credit limit that you are allowed is another consideration that you should make. The amount that you are allowed will normally be largely dependent on your credit rating, but different providers will offer you different amounts and the same provider may offer you different amounts under different credit card deals.

As an indication, most credit cards in the UK have a limit of between £3,000 and £4,000. If you have a poor credit rating, your limit may be as low as £200 and if you have a very good credit rating, it can be in the tens of thousands of pounds.

Balance Transfer Fees

If you are looking to transfer the balance from a credit card which is accruing interest onto a different card, then the balance transfer fees are the key thing to look at. The best thing to look for is a balance transfer credit card. While there are normally still fees involved for making transfers, these cards can often help to save you money in the long run.

Visa Or Mastercard?

Some people wonder whether they should opt for a Visa or Mastercard credit card. There is not much difference between Visa and Mastercard. Both are widely accepted around the world, and these two payment systems have no direct effect on the interest rate or rewards that you will get from your credit card provider. That said, sometimes there can be perks for credit card customers which come from having a credit card with either Visa or Mastercard. In the UK, Visa and Mastercard are the most widely accepted transaction handlers and either will make a good choice.

Fixed Rate vs Variable Rate APR

Credit card APR rates come as fixed or variable. Here’s what you need to know:

Variable Rate APR

Variable APR rates do not change entirely at the discretion of your credit card provider, meaning that they can increase what they charge you to make profit. They change according to what is known as an ‘index rate’. This is normally the rate of inflation. As the economy fluctuates and interest rates change, the APR rate will change to take this into account. Most credit cards come with variable rate APR.

Fixed Rate APR

Fixed APR rates do not vary according to an index rate. Roughly speaking, the rate of interest that you pay will stay the same for the time that you borrow money. However, credit card companies can change the fixed rate of APR. Usually they will have to notify you of a change and changes to interest rates will only apply to money that you borrow after you have been notified of the change.

Our Top 5 Credit Cards

Here are Cashfloat’s top 5 credit cards on offer in the UK. For a recap on the different types of credit card (such as purchase or balance transfer card) go to Chapter 6 of this guide.

- Lloyds Bank 0% Purchase and Balance Transfer Credit Card

This credit card offers 0% interest on purchases for the first 21 months and a representative APR of 21.9%, making it a great purchase card. It can also be used as a balance transfer card, with 19 months with no interest or fees. - Barclays Platinum with Balance Transfer

Competing very closely with Lloyds Bank’s flagship card, this is a great purchase credit card with 0% interest for the first 20 months and representative APR of 21.9%. It can also be used as a balance transfer card, with 19 months with no interest or fees. - Chrome Credit Card

This is a good credit builder credit card for those with a poor credit rating or no credit history. Credit limits start at manageable amounts of between £250 and £1500, but can be built up to £4,000 over time. Representative APR is 29.5%. - American Express Platinum Cashback Everyday Credit

For people who find that they do want to take a rewards credit card, American Express often have the best offers. This card gives up to 5% cashback on purchases made in the first 3 months of membership, up to a maximum of £100. After that 1% cashback is given. The card is also a good purchase card, with a representative APR of 22.9%.

Should you Take Out a Credit Card?

Before you decide to take out a credit card, you should think about whether you really need one. Do you need access to credit or to build your credit score, or do you just fancy having access to some extra money? Go to Chapter 5 of this guide for an in depth look at the advantages and disadvantages to having a credit card.

You should make a plan as to whether you intend to pay off the whole balance each month or to spread the cost of paying for a large purchase over several months or even years. You should consider exactly how you will find the money to pay your extra bills and you should think about what would happen if you faced financial difficulty, such as being made redundant. Taking out a credit card will leave you with a bill that you will have to pay off and it is important that you make the right decision.

Will I be Eligible for a Credit Card?

If you decide that you do want to take out a credit card, you will need to make an application. Your credit score is the most important thing that will affect your eligibility to receive a credit card.

Your Credit Score

Your credit history is used to determine your credit score, otherwise known as your credit rating. Your credit score is the most important thing affecting your application for a credit card. The lower your credit rating, the higher the rate of interest you are likely to be offered and the lower your credit limit is likely to be. If you have a poor credit rating you might be turned down altogether when you make an application. On the other hand, if you have a good credit rating, you may be offered favourable borrowing conditions.

There is much more information about credit scoring and credit history in Chapter 12 of this guide. However, it is important to understand that your credit rating will have an influence on a credit card application.

Use a Credit Card Calculator First

If you are not sure whether your application for a credit card will be successful, one useful tip is to use a credit card comparison tool first. As well as telling you what cards are available, these will often also give you an indication of whether your application will be successful. Sending off multiple applications for credit cards is often seen as a mark of desperation and can arouse suspicion amongst credit card providers. This in turn can lead them to inquire into your credit history and having had enquiries made into your credit history may adversely affect your credit rating.

The calculators are simple to use. Just enter any details that affect your application such as your income and outgoings, and any current debts. The results will be shown as a soft search which other lenders do not see on your credit file. After you are more informed on what is available to you, you will be able to make targeted credit card applications.

Summary: How to Compare Credit CardsWhile all of this information may be a lot to take in, hopefully it will help you to understand more about how to compare credit cards and the deals that are on offer. Take your time to look at everything available and make sure that you read the smallprint. Do not jump straight in and apply for the first low rate card that you see.

Plan your payments ahead of time, taking into account interest rates. Remember that introductory offers only last as long as the introductory period and when it comes to rewards and incentives, consider whether these will actually be financially beneficial. Choosing the right credit card takes research, and this takes time.

The next chapter in this series, by Cashfloat, looks at charge cards. We will explain how charge cards work, who should apply for one and who the best providers are.